Five reasons why it’s vital to review your liability insurance Limits of Indemnity

Allianz estimate that inflationary factors have more than doubled liability claims costs over the last 10 years. Within that timeframe many businesses haven’t changed the Limit of Indemnity provided by their liability insurance policies, leaving themselves exposed to potentially catastrophic underinsurance.

Here are some key factors driving claims cost inflation:

- The “Ogden rate” https://en.wikipedia.org/wiki/Ogden_tables used to assess damages awards now assumes that claims lump sum payments earn a negative interest rate.

Up until March 2017 a positive rate of 2.5% was used for this calculation. After 17 months at -0.75% the rate changed to -0.25% in August 2019.

This means a bigger lump sum payment is needed to fund long term loss of earnings, or increased living costs resulting from an injury. - The Introduction of new regulations such as The Equality Act and GDPR have broadened the scope of cover provided.

- Improved medical care means that life expectancy is increasing, so awards need to fund care for longer periods.

- This improved medical care comes at a cost, and the increasing cost of treatment also drives claims inflation.

- People are typically retiring later, lengthening the amount of time they need to be compensated for in lost earnings.

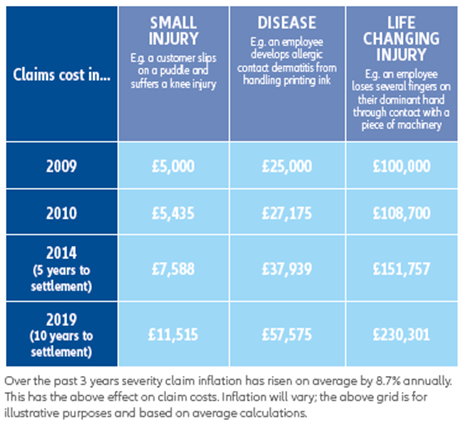

Allianz recently published some examples:

So what do you need to do?

Make sure you have the cover you need! - speak to your local GRP broker for expert advice on your liability insurance coverage and limits of indemnity.